Note

Go to the end to download the full example code.

Smooth Quantile Regression with QuantileHuber#

This example compares sklearn’s standard quantile regression with skglm’s smooth approximation. Skglm’s quantile regression uses a smooth Huber-like approximation (quadratic near zero, linear in the tails) to replace the non-differentiable pinball loss. Progressive smoothing enables efficient gradient-based optimization, maintaining speed and accuracy also on large-scale, high-dimensional datasets.

# Author: Florian Kozikowski

import numpy as np

import time

import matplotlib.pyplot as plt

from sklearn.datasets import make_regression

from sklearn.linear_model import QuantileRegressor

from skglm.experimental.quantile_huber import QuantileHuber, SmoothQuantileRegressor

# Generate regression data

X, y = make_regression(n_samples=1000, n_features=10, noise=0.1, random_state=0)

tau = 0.8 # 80th percentile

Compare standard vs smooth quantile regression#

Both methods solve the same problem but with different loss functions.

# Standard quantile regression (sklearn)

start = time.time()

sk_model = QuantileRegressor(quantile=tau, alpha=0.1)

sk_model.fit(X, y)

sk_time = time.time() - start

# Smooth quantile regression (skglm)

start = time.time()

smooth_model = SmoothQuantileRegressor(

quantile=tau,

alpha=0.1,

delta_init=0.5, # Initial smoothing parameter

delta_final=0.01, # Final smoothing (smaller = closer to true quantile)

n_deltas=5 # Number of continuation steps

)

smooth_model.fit(X, y)

smooth_time = time.time() - start

Evaluate both methods#

Coverage: fraction of true values below predictions (should ≈ tau) Pinball loss: standard quantile regression evaluation metric

Note: No robust benchmarking conducted yet. The speed advantagous likely only shows on large-scale, high-dimensional datasets. The sklearn implementation is likely faster on small datasets.

def pinball_loss(residuals, quantile):

return np.mean(residuals * (quantile - (residuals < 0)))

sk_pred = sk_model.predict(X)

smooth_pred = smooth_model.predict(X)

print(f"{'Method':<15} {'Coverage':<10} {'Time (s)':<10} {'Pinball Loss':<12}")

print("-" * 50)

print(f"{'Sklearn':<15} {np.mean(y <= sk_pred):<10.3f} {sk_time:<10.3f} "

f"{pinball_loss(y - sk_pred, tau):<12.4f}")

print(f"{'SmoothQuantile':<15} {np.mean(y <= smooth_pred):<10.3f} {smooth_time:<10.3f} "

f"{pinball_loss(y - smooth_pred, tau):<12.4f}")

Method Coverage Time (s) Pinball Loss

--------------------------------------------------

Sklearn 0.799 0.058 28.2682

SmoothQuantile 0.798 2.373 28.2699

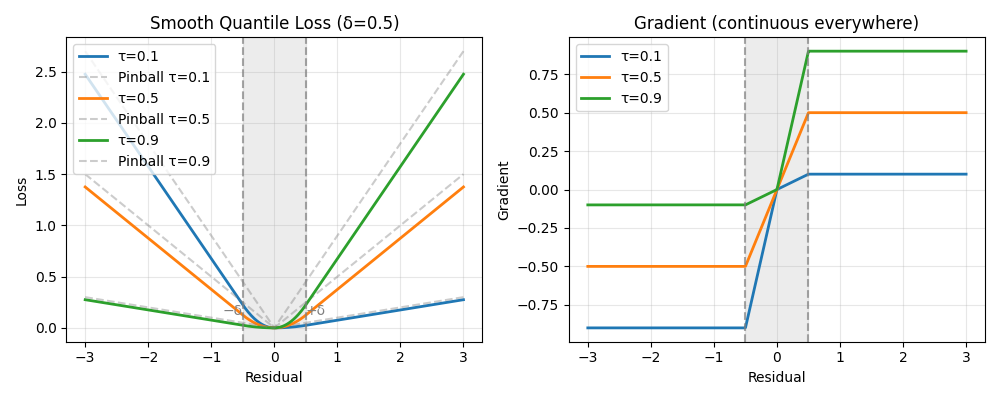

Visualize the smooth approximation#

The smooth loss approximates the pinball loss but with continuous gradients

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(10, 4))

# Show loss and gradient for different quantile levels

residuals = np.linspace(-3, 3, 500)

delta = 0.5

quantiles = [0.1, 0.5, 0.9]

for tau_val in quantiles:

qh = QuantileHuber(quantile=tau_val, delta=delta)

loss = [qh._loss_sample(r) for r in residuals]

grad = [qh._grad_per_sample(r) for r in residuals]

# Compute pinball loss for each residual

pinball_loss = [r * (tau_val - (r < 0)) for r in residuals]

# Plot smooth loss and pinball loss

ax1.plot(residuals, loss, label=f"τ={tau_val}", linewidth=2)

ax1.plot(residuals, pinball_loss, '--', alpha=0.4, color='gray',

label=f"Pinball τ={tau_val}")

ax2.plot(residuals, grad, label=f"τ={tau_val}", linewidth=2)

# Add vertical lines and shading showing delta boundaries

for ax in [ax1, ax2]:

ax.axvline(-delta, color='gray', linestyle='--', alpha=0.7, linewidth=1.5)

ax.axvline(delta, color='gray', linestyle='--', alpha=0.7, linewidth=1.5)

# Add shading for quadratic region

ax.axvspan(-delta, delta, alpha=0.15, color='gray')

# Add delta labels

ax1.text(-delta, 0.1, '−δ', ha='right', va='bottom', color='gray', fontsize=10)

ax1.text(delta, 0.1, '+δ', ha='left', va='bottom', color='gray', fontsize=10)

ax1.set_title(f"Smooth Quantile Loss (δ={delta})", fontsize=12)

ax1.set_xlabel("Residual")

ax1.set_ylabel("Loss")

ax1.legend(loc='upper left')

ax1.grid(True, alpha=0.3)

ax2.set_title("Gradient (continuous everywhere)", fontsize=12)

ax2.set_xlabel("Residual")

ax2.set_ylabel("Gradient")

ax2.legend(loc='upper left')

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

The left plot shows the asymmetric loss: tau=0.1 penalizes overestimation more, while tau=0.9 penalizes underestimation. As delta decreases towards zero, the loss function approaches the standard pinball loss. The right plot reveals the key advantage: gradients transition smoothly through zero, unlike standard quantile regression which has a kink. This smoothing enables fast convergence with gradient-based solvers.

Total running time of the script: (0 minutes 2.707 seconds)